Due to the COVID-19 relief bill signed in December 2020, employers have new options for the 2020 and 2021 plan years regarding rollovers and grace periods.

FSA Rollovers: Plans may permit unused funds in medical or dependent care FSA plans to completely rollover from 2020 into 2021, and 2021 into 2022. If this option is chosen, the standard $550 rollover max will not apply for these plan years.

FSA Grace Period: Plans may permit a 12-month grace period for unused benefits for plan years ending in 2020 or 2021.

If you have any questions, please contact us.

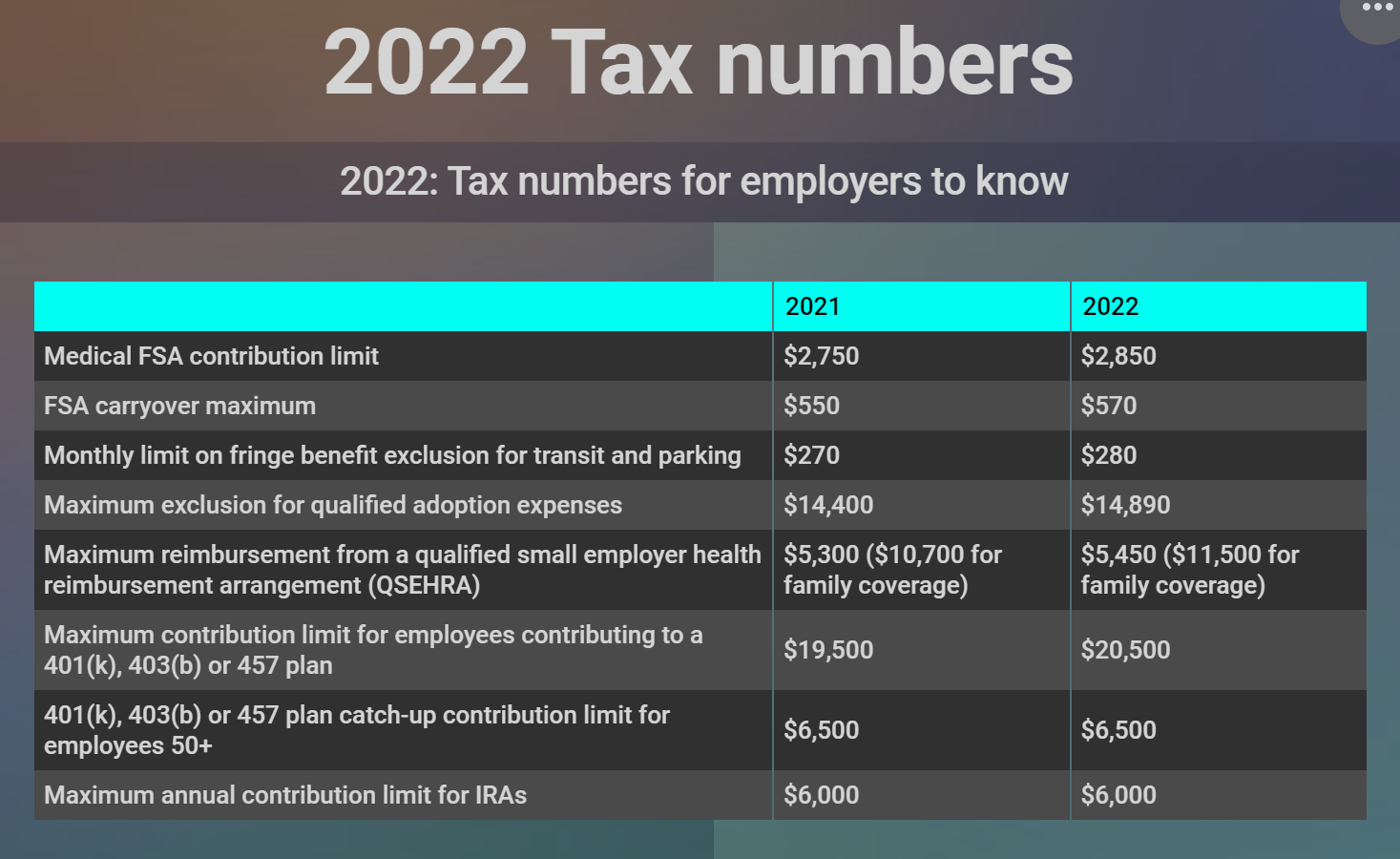

You can offer your employees the ability to rollover up to $550 of their medical Flexible Spending Account (FSA) into the following year. This IRS rule has been in place since 2013 and has helped make FSAs a more attractive account for employees.

The basics

It's important to note that FSAs don't automatically rollover unless you set the plan up to do so. If you don't choose the rollover option, any remaining employee funds at the end of the year will be forfeited from their accounts. However, employees do not need to elect to rollover the money. If it's in their account at the end of the year and you've set it up to rollover, it will automatically rollover.

The rollover amount does not count toward the annual FSA contribution limit. As a result, an employee can elect the full annual amount and still go over that amount by up to $550 if that much is left over.

Anything in the employee account over $550 at the end of the year will be forfeited, as will any balance if the employee resigns or is terminated.

Your standard fees will apply to all current FSA accounts whether or not the balance is due to an election or rollover dollars only.

The run-out period and grace period

During the run-out period (the time following the end of the plan year when employees can still submit expenses made in the previous plan year), the rollover amount is available to use for dates of service both from the prior plan year and service from the new plan year.

After the run-out period, the rollover amount will no longer be available to apply to service from the previous year. The remaining rollover balance will now only be considered part of the current year's balance.

However, a plan with a rollover option cannot have a grace period. This is how a grace period differs from a run-out period:

- The grace period allows employees to spend down their balance from the previous year on expenses made in the new year

- The IRS caps a grace period at 2.5 months, whereas the run-out period length is chosen by the employer (the standard is 3 months)

- If an employee has a medical FSA and HSA, the employee can't make HSA contributions during the grace period. HSA contributions can't be made until the first day of the month following the end of the grace period. However, employees covered under a limited purpose or post-deductible FSA are allowed to contribute to HSAs. A run-out period does not impact anyone's ability to contribute to an HSA

Source: https://learn.hellofurther.com/Employers/Group_Administration/What_to_Know_About_FSA_Rollovers